The ACH network processed 33.6 billion payments worth $86.2 trillion in 2024 (Nacha, 2025). That is roughly 100 million transactions every single day. Ninety-three percent of American workers receive their paychecks through it. Ninety-nine percent of Social Security payments flow through it. Over 90% of tax refunds land in bank accounts via ACH (Nacha, 2025).

Yet for a system this critical, ACH remains poorly understood. Most articles define it in a sentence, list a few benefits, and move on. This article goes deeper. It covers how ACH actually works at a technical level, the economics that make it indispensable for businesses, the fraud landscape, how it compares to wire transfers, cards, and real-time payment rails, and how Juspay Hyperswitch helps businesses integrate ACH alongside 300+ processors and payment methods through a single API.

What Is ACH, and Why Does It Exist?

ACH stands for Automated Clearing House. It is an electronic funds transfer system that moves money between bank accounts across the United States. The network is governed by Nacha (National Automated Clearing House Association), which writes and enforces the operating rules every participating financial institution must follow.

ACH was created in the early 1970s as a digital alternative to paper checks. The Federal Reserve and a consortium of California banks built the first clearing house in 1972. The goal was straightforward: replace the physical movement of billions of paper checks with electronic batch processing.

Today, two operators process ACH transactions:

- The Federal Reserve (FedACH): Operated by the Federal Reserve Banks, processing the majority of ACH volume

- EPN (Electronic Payments Network): Operated by The Clearing House, a private-sector payment company owned by large commercial banks

Both operators interoperate. A transaction originated through one can settle through the other, so the network functions as a single system from the end user's perspective.

How ACH Transactions Actually Work: The Full Lifecycle

ACH is a batch-processing system, not a real-time network. Transactions are collected, grouped, and processed in windows throughout the day. Here is the step-by-step flow:

Step 1: Origination

A company or individual (the "Originator") initiates a payment. This could be a payroll direct deposit, a recurring subscription charge, or a one-time bill payment. The Originator submits the transaction to their bank, called the Originating Depository Financial Institution (ODFI).

Step 2: Batching

The ODFI collects multiple ACH entries into a batch file formatted according to Nacha's specifications. Each entry includes the routing number, account number, transaction amount, and Standard Entry Class (SEC) code that indicates the type of transaction.

Step 3: Transmission to ACH Operator

The ODFI transmits the batch to one of the two ACH operators (FedACH or EPN). Operators receive files at scheduled windows throughout the business day.

Step 4: Sorting and Distribution

The ACH operator sorts all incoming entries by the Receiving Depository Financial Institution (RDFI) and creates outgoing files for each receiving bank.

Step 5: Settlement

The RDFI receives the entries, posts the credits or debits to customer accounts, and the Federal Reserve settles the net amounts between banks. Standard ACH settles in one to two business days. Same-Day ACH settles within the same business day.

Step 6: Returns (If Applicable)

If a transaction cannot be completed (insufficient funds, invalid account, authorization revoked), the RDFI generates a return entry. Returns must be submitted within two business days for most return codes.

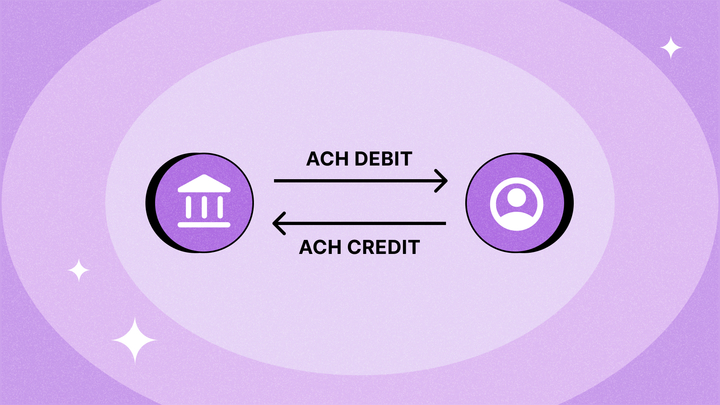

The Two Types of ACH Transactions

| Type | Direction | Who Initiates | Common Uses |

| ACH Credit | Money pushed from sender to receiver | The payer | Payroll direct deposits, vendor payments, tax refunds |

| ACH Debit | Money pulled from payer's account | The payee/collector | Subscription billing, mortgage payments, utility bills, insurance premiums |

This push/pull distinction matters. ACH credits carry lower fraud risk because the sender controls the payment. ACH debits require prior authorization from the account holder, and fraudulent debits are the primary vector for ACH-related fraud.

Standard Entry Class (SEC) Codes: The Taxonomy of ACH Payments

Every ACH transaction carries a three-letter SEC code that tells the network what type of payment it is and what authorization rules apply. These codes are not cosmetic. They determine regulatory requirements, return timeframes, and fraud liability.

| SEC Code | Name | Use Case | Authorization |

| PPD | Prearranged Payment and Deposit | Payroll, direct deposit, recurring consumer payments | Written or electronic authorization |

| CCD | Corporate Credit or Debit | B2B payments between companies | Written agreement |

| WEB | Internet-Initiated Entry | Online payments, e-commerce | Internet-based authorization |

| TEL | Telephone-Initiated Entry | Payments authorized over the phone | Recorded verbal authorization |

| CTX | Corporate Trade Exchange | B2B payments with addenda records (invoices, remittance data) | Written agreement |

| IAT | International ACH Transaction | Cross-border ACH payments | Varies by country |

| RCK | Re-presented Check Entry | Converting a returned check to electronic | Original check serves as authorization |

Understanding SEC codes is essential for compliance. Using the wrong code for a transaction type can result in Nacha rule violations and financial penalties.

The Economics of ACH: Why Businesses Rely on It

ACH dominates for one reason above all others: cost.

Transaction Cost Comparison

| Payment Method | Typical Cost Per Transaction | Settlement Speed |

| ACH | $0.20 to $1.50 | 1 to 2 business days (standard), same day available |

| Credit Card | 1.5% to 3.5% of transaction value | 1 to 3 business days |

| Debit Card | $0.21 + 0.05% (regulated) | 1 to 2 business days |

| Wire Transfer | $15 to $30 (domestic) | Same day or next day |

| RTP/FedNow | $0.01 to $1.00 | Seconds |

For a $5,000 B2B invoice payment, the math is stark:

- ACH: ~$0.50

- Credit card at 2.5%: $125

- Wire transfer: $25

That is a 250x cost difference between ACH and credit card for the same transaction. For businesses processing thousands of payments monthly, ACH saves hundreds of thousands of dollars per year in processing fees alone.

Where ACH Dominates

- Payroll: 93% of American workers receive pay via ACH direct deposit (Nacha, 2025)

- Government payments: 99% of Social Security benefits, 90.6% of tax refunds (Nacha, 2025)

- B2B payments: The fastest-growing ACH segment, as businesses move away from paper checks

- Recurring billing: Subscription services, insurance premiums, mortgage payments, utility bills

- Account-to-account transfers: P2P apps and bank transfers between a consumer's own accounts

Same-Day ACH: The Network Gets Faster

When Nacha launched Same-Day ACH in 2016, it addressed the biggest criticism of the network: speed. Instead of waiting one to two business days, Same-Day ACH enables settlement within hours.

How Same-Day ACH Works

Same-Day ACH uses the same infrastructure as standard ACH but with additional processing windows. As of 2025, there are three same-day processing windows:

| Window | Submission Deadline (ET) | Settlement Time (ET) |

| Window 1 | 10:30 AM | 1:00 PM |

| Window 2 | 2:45 PM | 5:00 PM |

| Window 3 | 4:45 PM | By end of day |

Transaction Limits

The per-transaction limit for Same-Day ACH is currently $1 million, raised from $100,000 in stages over several years. This increase opened the door for larger B2B payments to use same-day settlement.

Volume Growth

Same-Day ACH volume has grown rapidly since launch. The service processed 893 million payments worth $2.8 trillion in 2024, representing continued double-digit year-over-year growth (Nacha). Same-day transactions now represent a meaningful share of total ACH volume, demonstrating that businesses and consumers value faster settlement.

ACH Return Codes: What Happens When Transactions Fail

Not every ACH transaction completes successfully. When a receiving bank cannot process a transaction, it sends a return with a specific code indicating the reason. Understanding return codes is critical for managing payment operations.

Most Common Return Codes

| Code | Reason | What It Means | Action Required |

| R01 | Insufficient Funds | Account exists but doesn't have enough money | Retry after confirming funds, or contact customer |

| R02 | Account Closed | The bank account has been closed | Obtain new payment information |

| R03 | No Account/Unable to Locate | Account number doesn't match any account at that bank | Verify account and routing numbers |

| R04 | Invalid Account Number | Account number structure is invalid | Correct the account number |

| R05 | Unauthorized Debit | Account holder did not authorize the debit | Investigate and resolve with customer |

| R07 | Authorization Revoked | Customer revoked a previously given authorization | Stop future debits to this account |

| R08 | Payment Stopped | Account holder placed a stop payment | Contact customer for resolution |

| R10 | Customer Advises Unauthorized | Customer claims they did not authorize the transaction | High fraud risk, investigate immediately |

| R20 | Non-Transaction Account | Account type (e.g., savings) doesn't permit this transaction | Use correct account type |

| R29 | Corporate Customer Advises Not Authorized | Corporate account holder denies authorization | Investigate, potential fraud |

Return Timeframes

- R01 to R04 (administrative returns): RDFI has two business days to return

- R05, R07, R10, R29 (unauthorized returns): Consumer has 60 calendar days to dispute

- R05 specifically for CCD/CTX entries: Two business days

A high return rate is a red flag for payment processors and Nacha. If an originator's unauthorized return rate exceeds 0.5% (overall) or 0.5% (administrative), they may face monitoring, fines, or termination from the network.

ACH Fraud: The $11 Billion Problem

ACH fraud is growing. In 2024, ACH fraud-related returns cost U.S. financial institutions an estimated $11 billion (AFP Payments Fraud and Control Survey, 2025). Thirty-eight percent of organizations experienced ACH debit fraud, and 20% were victims of ACH credit fraud.

How ACH Fraud Happens

Business Email Compromise (BEC) remains the dominant attack vector. Fraudsters impersonate vendors, executives, or partners to trick finance teams into initiating ACH payments to fraudulent accounts. In 2024, 50% of BEC-targeted payments used ACH credits (AFP, 2025).

Unauthorized debits occur when bad actors obtain bank account and routing numbers (which are far easier to steal than card numbers, since they are printed on every check) and initiate unauthorized ACH pulls.

Account takeover involves gaining access to online banking portals or payment platforms to originate fraudulent ACH transactions.

Nacha's Fraud Prevention Framework

Nacha has implemented several rules to combat fraud:

- ACH Debit Monitoring: Since 2024, all RDFIs must monitor incoming ACH debits for anomalies

- Account Validation Rule: Requires originators of WEB debit entries to validate account ownership using commercially reasonable methods

- Nacha Risk Management Framework: Sets thresholds for unauthorized return rates and requires remediation when exceeded

- Micro-deposit verification: Sending small test deposits to confirm account ownership before large transactions

Best Practices for Businesses

- Implement ACH Positive Pay: Allow your bank to compare incoming ACH debits against an approved list

- Use ACH Debit Blocks/Filters: Block all ACH debits except from pre-approved originators

- Verify accounts before originating: Use account validation APIs to confirm account ownership

- Monitor return codes: R05, R07, R10, and R29 returns signal potential fraud and require investigation

- Segregate duties: The person who creates ACH payments should not be the same person who approves them

ACH vs. Wire Transfers vs. Cards vs. Real-Time Payments

Each payment rail serves different needs. Choosing the right one depends on urgency, transaction size, cost sensitivity, and use case.

Detailed Comparison

| Feature | ACH | Wire Transfer | Credit/Debit Card | RTP | FedNow |

| Speed | 1-2 days (standard), same day available | Same day, often within hours | 1-3 day settlement | Seconds | Seconds |

| Cost | $0.20 to $1.50 | $15 to $30 domestic, $35 to $50 international | 1.5% to 3.5% | $0.01 to $1.00 | $0.01 to $0.045 |

| Transaction Limit | $1M (same-day), no limit (standard) | No limit | Varies by issuer | $1 million | $500,000 |

| Reversibility | Yes, within return windows | Generally irreversible | Chargebacks available | Irreversible | Irreversible |

| Availability | Business days only | Business days only | 24/7 authorization | 24/7/365 | 24/7/365 |

| Best For | Recurring, batch, payroll, B2B | Urgent high-value transfers | Consumer purchases, e-commerce | Urgent business payments | Instant consumer/business payments |

| Operator | FedACH, EPN | Federal Reserve (Fedwire), CHIPS | Visa, Mastercard networks | The Clearing House | Federal Reserve |

| Network Reach | All U.S. banks | All U.S. banks | Global | ~800 FIs (2025) | ~1,500 FIs (2025) |

When to Use What

- ACH when cost matters most and same-day or next-day settlement is acceptable. Payroll, B2B invoices, recurring billing, subscription payments.

- Wire when you need guaranteed same-day finality for high-value transactions. Real estate closings, large corporate transactions, time-sensitive M&A payments.

- Cards when the payer is a consumer making a purchase and expects rewards, chargebacks, and a familiar checkout experience.

- RTP/FedNow when you need instant confirmation and finality. Gig worker payouts, insurance claims, urgent B2B payments, account funding.

The Relationship Between ACH, RTP, and FedNow

A common question: will real-time payment rails replace ACH? The short answer is no, not for the foreseeable future.

RTP (operated by The Clearing House) and FedNow (operated by the Federal Reserve) complement ACH rather than compete with it. Each system serves different use cases:

- ACH excels at high-volume, low-cost batch processing. Payroll for 100,000 employees, subscription billing for millions of customers, and B2B payment runs are precisely what ACH was built for. The per-transaction cost is unbeatable at scale.

- RTP and FedNow handle urgent, low-volume payments where instant confirmation matters. By end of 2025, approximately 1,500 financial institutions had joined FedNow, a faster adoption rate than RTP achieved in its early years.

The practical reality is that businesses need multiple payment rails. A company might use ACH for payroll and vendor payments, RTP for emergency disbursements, wire transfers for large real estate transactions, and cards for customer-facing commerce. The challenge is managing all of these through a unified infrastructure.

International ACH (IAT): Cross-Border Payments

ACH is not limited to domestic transactions. International ACH Transactions (IATs) enable cross-border payments through the same network, with additional compliance requirements.

In 2024, international ACH processed $270.96 billion in value across 120.99 million payments, representing a 64% increase over recent years (Nacha). For context, this is up from 73.66 million transactions in 2015.

How IAT Works

IATs use the same ACH infrastructure but carry additional data fields for:

- Foreign bank identification: SWIFT/BIC codes or national bank identifiers

- Originator and receiver country codes: For sanctions screening

- Foreign exchange information: When currency conversion is involved

- Enhanced OFAC/sanctions screening: Required for all IAT entries

2025 Rule Changes

Nacha approved five significant changes to IAT rules in 2025, the first major revisions since 2009:

- Clearer definitions of what qualifies as an international ACH transaction

- Requirement to include date of birth for enhanced sanctions screening

- Simplified distinction between sanctions-related rejections and other return reasons

- Recognition that non-U.S. financial institutions can operate as non-traditional account holders

- U.S. financial institutions must register IAT-specific contacts in Nacha's Contact Registry

Regulatory Framework: Who Governs ACH?

ACH operates under multiple layers of regulation:

Nacha Operating Rules

Nacha is the self-regulatory body that governs the ACH network. Its operating rules cover:

- Transaction formatting and processing requirements

- Authorization requirements for each SEC code

- Return timeframes and procedures

- Risk management and fraud prevention

- Fines and penalties for rule violations

Federal Regulations

- Electronic Fund Transfer Act (EFTA): Protects consumers in electronic fund transfers, including ACH. Limits consumer liability for unauthorized transfers.

- Regulation E (implementing EFTA): Requires disclosure of terms, error resolution procedures, and limits on consumer liability. Consumers have 60 days to report unauthorized ACH debits.

- Regulation CC: Governs fund availability for ACH credits

- Bank Secrecy Act (BSA)/Anti-Money Laundering (AML): Requires monitoring and reporting of suspicious ACH activity

- OFAC Compliance: All ACH transactions must be screened against OFAC sanctions lists, with enhanced requirements for IAT entries

How Juspay Hyperswitch Handles ACH Payments

Juspay Hyperswitch provides end-to-end ACH capabilities through a single API, covering verification, payment collection, recurring mandates, and payouts. Here is exactly what the platform supports.

ACH Bank Debit: Collecting Payments

Juspay Hyperswitch supports ACH bank debit as a first-class payment method under the bank_debit category. Customers provide their bank account number, routing number, account holder name, and bank type (Checking or Savings), then authorize a mandate allowing the merchant to debit their account.

Supported processors for ACH debit:

| Processor | Zero-Mandate | Regular Mandate | Required Fields |

| Stripe | Yes | Yes | Billing name, account number, routing number |

| Adyen | Yes | Yes | Billing name, account number, routing number |

| GoCardless | Yes | Yes | Account details, mandate authorization |

| Payload | Yes | Yes | Billing zip, account number, routing number, holder name, bank type |

| Dwolla | Yes | Yes | Billing name, account number, routing number, holder name, bank type |

Since ACH direct debit is a delayed notification payment method, it can take up to 4 business days for the payment status to be updated.

ACH Verification

Before debiting a bank account, the account must be verified. Juspay Hyperswitch supports two verification approaches:

- Micro-deposit verification (via Stripe): Two small test deposits are sent to the customer's bank account. The customer confirms the amounts to prove account ownership. This takes 1 to 2 business days but works with any US bank account.

- Instant bank verification: Customers link their bank account through a real-time verification flow, confirming ownership instantly without waiting for test deposits.

Recurring Payments and Mandates

ACH's lowest-cost advantage shows up most clearly in recurring billing. Juspay Hyperswitch implements recurring ACH through the mandate system:

- Initial setup: The customer provides bank details and authorizes a mandate via mandate_data in the payment creation request, specifying customer_acceptance (online with IP address and user agent) and mandate_type (single_use or multi_use).

- Subsequent charges: Once the mandate is active, the merchant can initiate recurring debits against the stored authorization without requiring the customer to re-enter details.

- Processor-agnostic tokenization: Bank account details are securely stored in Juspay Hyperswitch's independent vault, meaning merchants can switch ACH processors without asking customers to re-authorize.

This covers subscription billing, insurance premiums, rent collection, loan repayments, and any use case where a business needs to pull funds from a customer's bank account on a recurring basis.

ACH Payouts: Sending Money

Juspay Hyperswitch also supports ACH on the payout side, enabling businesses to disburse funds to bank accounts via ACH transfer. Supported payout processors for ACH bank rails include Adyen, Stripe, and Wise.

Payout capabilities include:

- Smart routing: Route payouts to the optimal processor based on cost, success rate, and geography

- Smart retries: If a payout fails due to a temporary connector error, Juspay Hyperswitch automatically retries through the most viable path (up to 5 retries per connector by default)

- Bulk operations: Upload .xlsx or .csv files via the dashboard for large-scale disbursements

- Payout links: Generate shareable links that allow recipients to enter their own bank details and receive funds in their preferred method

Smart Routing Across Payment Rails

Juspay Hyperswitch routes ACH transactions to the optimal processor using three routing strategies:

- Volume-based routing: Distribute a percentage of ACH traffic across multiple processors

- Rule-based routing: Create conditional logic (if currency = USD and amount > $10,000, route to Processor A)

- Default fallback routing: Establish a priority list so if the primary processor is unavailable, the system automatically routes to the next

Multi-Rail Strategy

The real power of Juspay Hyperswitch for ACH users is the ability to offer every payment rail through a single integration. Present ACH debit for recurring B2B invoices, cards for one-time consumer purchases, RTP for instant disbursements, SEPA for European customers, and BNPL for high-value consumer transactions. Juspay Hyperswitch connects to 300+ processors and payment methods, and the same API handles ACH, cards, wallets, bank redirects, and real-time payment rails.

Key Takeaways

ACH is the workhorse of American payments, processing over 33 billion transactions and $86 trillion annually. Its low cost, universal bank reach, and batch-processing efficiency make it irreplaceable for payroll, B2B payments, government disbursements, and recurring billing.

But ACH does not operate in isolation. Modern businesses need ACH alongside cards, wallets, real-time payments, and international methods. The operational complexity of managing multiple payment rails is the real challenge, and it is exactly what payment orchestration solves.

Juspay Hyperswitch provides a single API for ACH verification (micro-deposits and instant), ACH debit with recurring mandates, ACH payouts with smart retries, and 300+ processors and payment methods across every other rail. One integration. Every payment method. Full lifecycle coverage from verification through recurring collection to disbursement.