The benefits of network tokens are well-understood by now: stored card numbers, credentials leading to lesser PCI burden and updating themselves when a card is reissued, lower transaction costs and a few points of authorization-rate lift. The harder question, and the one that decides whether you actually capture that lift, is operational. Once you commit to network tokens, something has to happen on every single transaction, and someone has to own that work. Network tokens add work to every transaction, and someone has to do that work. This piece walks through how that work shrinks when a payment orchestrator owns it, and the benefits merchants pick up along the way.

From a merchant application's point of view, a tokenized payment is a single HTTP call. You send a request; you get back a result. Everything that makes tokenization work happens between those two events, and it is more than it looks.

An orchestration layer exists to own three things your application would otherwise own itself:

- Multi-party choreography: A single payment touches the card networks' token services, one or more acquirers, and a PCI-scoped vault. Each is a separate system with its own API and its own failure modes.

- Per-transaction state: A network token is not a credential you fetch once and reuse. Every authorization needs its own fresh, single-use cryptogram. The orchestrator generates one for each transaction and drives the transaction to completion.

- Failure recovery as policy: Tokenized transactions sometimes fail in ways a retry would fix. When the tokenization call fails, when to fall back from network token to card number, and when to give up all of it is intelligence that can be handled by an orchestrator.

The rest of this piece looks at what the orchestrator is actually doing when it owns the tokenization layer.

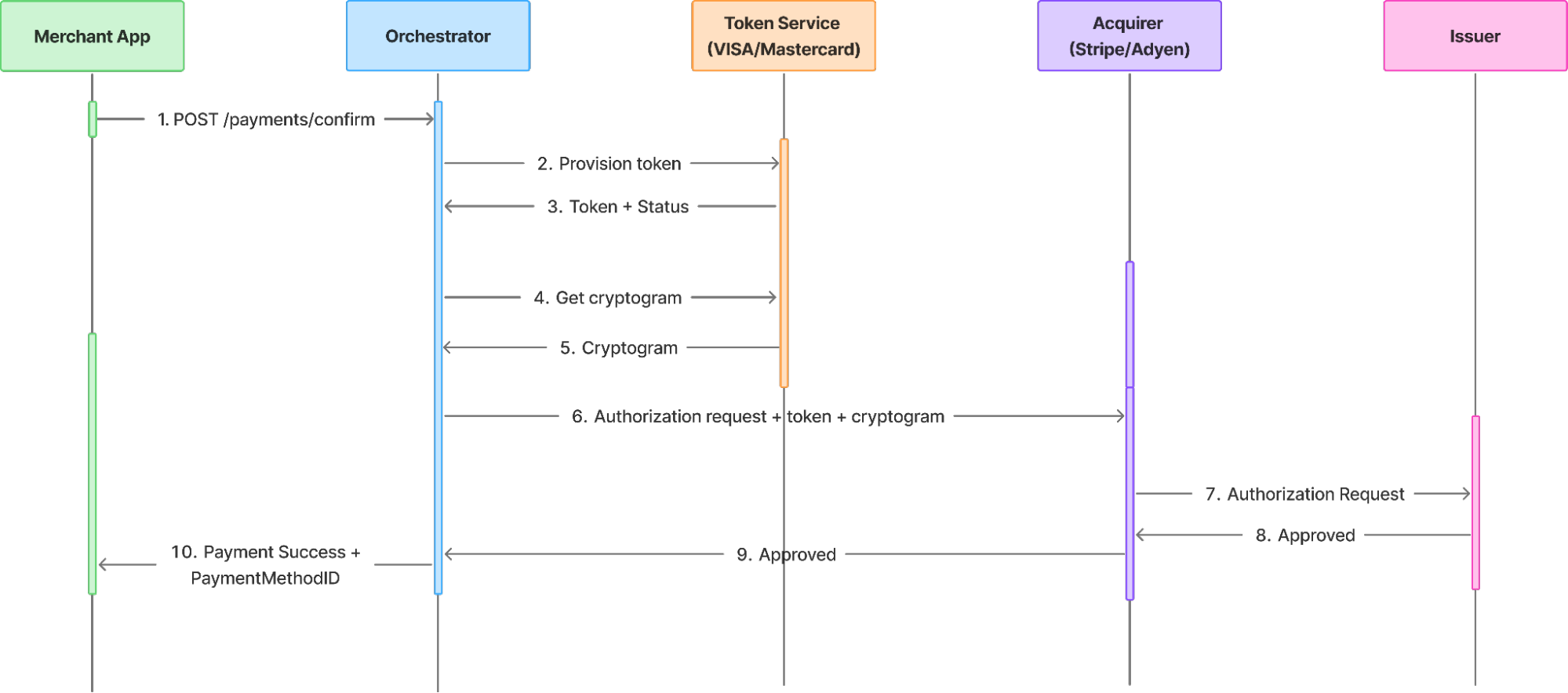

New user CIT payment

The first time a customer pays, your application sends raw card details to the orchestrator and waits for one response. The sequence diagram shows what happens in between.

Two parts of this sequence are worth separating. Provisioning the token asking the network's token service to issue a token for this card and generating a cryptogram asking for the one-time code that authorizes a specific transaction are two distinct API calls, not one combined operation. The orchestrator makes both, holds the results, assembles the authorization payload, sends it to the acquirer, and only then returns a result to your application, along with a payment method ID your application stores for next time. Eight internal messages; from where your application sits, one request and one response.

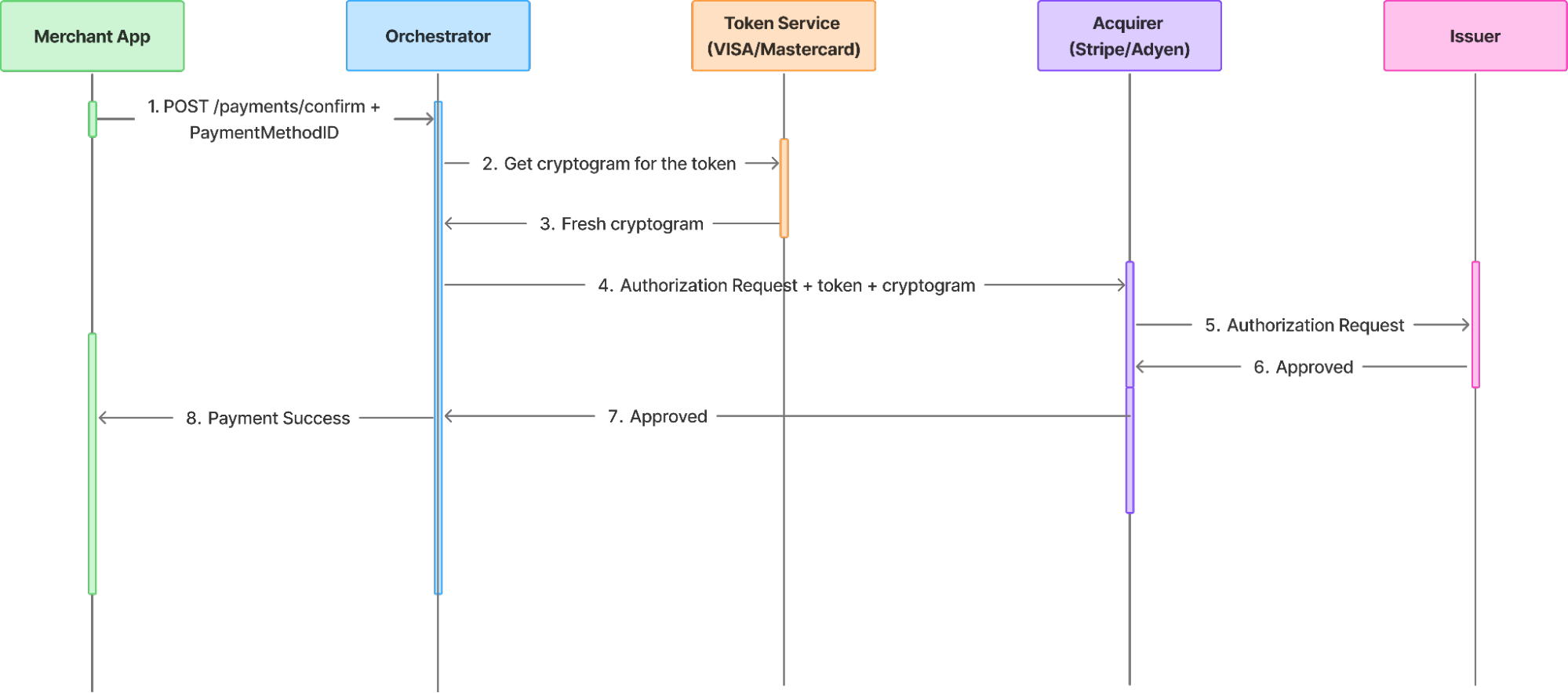

Repeat user CIT payment

The second payment is simpler. Your application passes the payment method ID from last time instead of card details. But notice what does not go away: the cryptogram step is still there.

Because cryptograms are single-use, the orchestrator cannot reuse the one from the first payment. It looks up which network token corresponds to that payment method ID, determines whether the card is a Visa or a Mastercard which decides whether it talks to Visa Token Service or Mastercard's MDES requests a fresh cryptogram, and shapes the authorization payload the way this particular acquirer expects it. The same token and cryptogram must be formatted differently for different acquirers. That translation is the orchestrator's job, and keeps it out of the merchant's application.

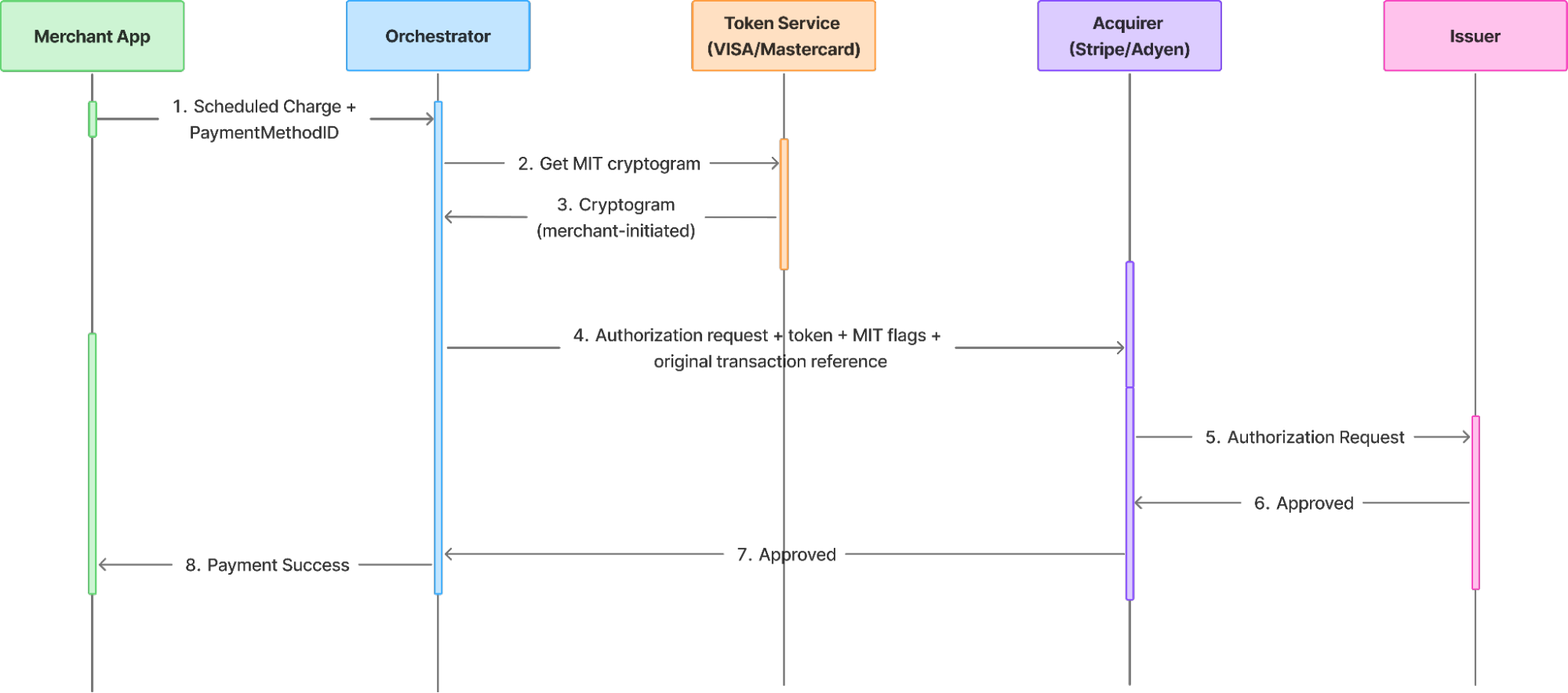

MIT payments

An MIT doesn't involve the cardholder at all. Your application tells the orchestrator to charge a stored payment method. The high-level shape looks like a repeat payment, but what changes underneath is that the cryptogram is a different kind, the authorization payload carries different flags.

Because the cardholder isn't present, the orchestrator requests a merchant-initiated cryptogram instead of a cardholder-present one, and stamps the authorization with the right scheme signals that this is a merchant-initiated charge and the kind (recurring, installment, unscheduled, no-show), and a reference back to the original cardholder-initiated transaction that established the mandate.

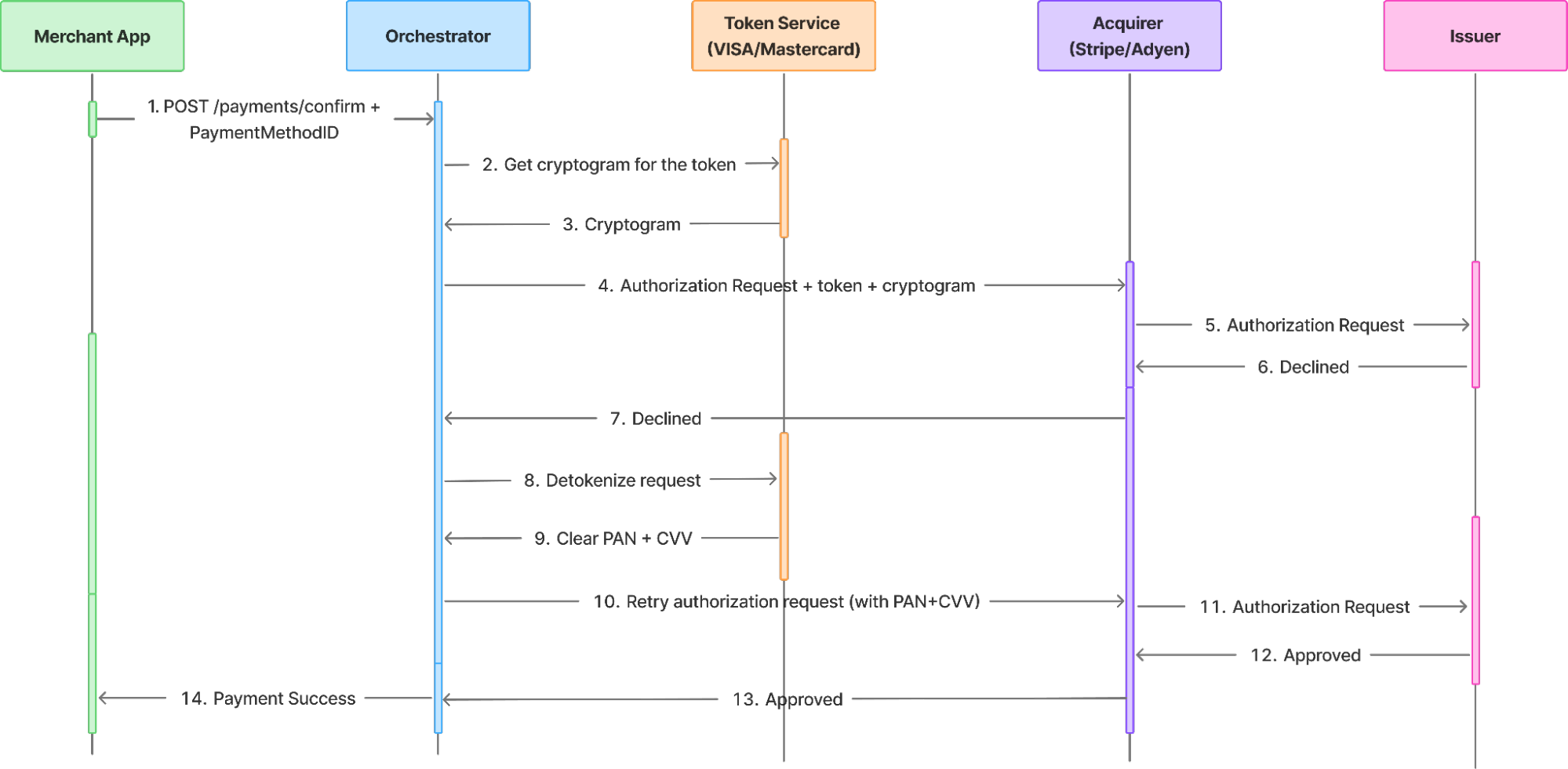

Transaction failure scenarios: when the token is declined

This is where an orchestration layer earns most of its value. Issuer fraud systems do not always score tokenized transactions as well as they score raw card numbers; many of those models were trained on card-number data and have less history with tokens. The result is that a transaction can be declined as a token when it would have been approved as a card number.

A capable orchestrator detects this, classifies the error as retriable or non-retriable, and within the retriable category tags it as a network token-to-PAN retry use-case retrieves the underlying card number from the vault, and retries the authorization all before returning anything to your application. From your application's point of view nothing unusual happened: the same request produced the same successful response, only slightly slower.

Replicating that behaviour without an orchestrator means your application would have to:

- Recognize a generic decline code as the specific kind that warrants a card-number retry, rather than a hard decline that should not be retried at all.

- Hold enough transaction state amount, currency, idempotency key to retry cleanly.

- Perform the detokenization itself, which puts your application back in PCI scope, the very thing tokenization was meant to avoid.

- Decide which retries are permitted, since not every merchant wants card-number fallback at all.

- Record which path each transaction took, so the value of tokenization can actually be measured.

Further responsibilities do not fit on a sequence diagram, where the orchestrator can help a merchant further are as below.

- Lifecycle events: Card networks emit asynchronous notifications, a token suspended, an underlying card reissued, an expiry updated that arrive hours or days after a payment. The orchestrator consumes these and updates its stored payment-method records, so the next transaction either works or fails fast instead of failing slowly.

- Multi-acquirer routing: When the orchestrator routes a transaction to a different acquirer/ a local acquirer in the cardholder's country, for instance the token has to remain valid there. Whether it does depends entirely on how the token was provisioned, which is the subject of the next section.

- Network divergence: Visa's and Mastercard's token systems are not symmetric. Their cryptograms have different formats, are generated through different APIs, and carry different lifecycle semantics. The orchestrator presents one uniform interface and absorbs that difference internally.

The decision that comes first: TRID ownership

Before any of the flows above can run, there is a structural decision to make and it is an easy one to make badly.

Network tokens are provisioned under a Token Requestor ID: a registration with the card network that identifies who asked for the token. Who holds that registration determines whether your tokens are portable. Three models are common:

- Shared TRID under a payment processor. Fast to set up the processor provisions tokens on your behalf. The cost is that those tokens are bound to that processor; route a transaction elsewhere and the token does not work.

- Dedicated TRID, operated for you. A vault or orchestration provider holds a TRID specifically for your business. The tokens are yours, and they work across any acquirer that accepts network tokens.

- Direct TRID ownership. You register with the networks yourself. Maximum control, maximum certification overhead that is hard to manage for a merchant mainly at large scale.

The implication for routing is direct. If you intend to use more than one acquirer and any merchant optimizing authorization rates, a shared processor TRID quietly removes that option. You capture the tokenization benefit on your primary processor and lose it the moment you route around it. Match the TRID model to the routing flexibility you want, and decide it before you provision a single token.

In short

An orchestration layer is worth a separate tier in your stack because network tokenization is not one feature, it is a set of obligations that recur on every transaction and compound across acquirers. The orchestrator owns the choreography, the per-transaction cryptogram state, and the failure-recovery policy, and it presents all of it to your application as a single, stable interface. Get the layer right, starting with TRID ownership, and the authorization-rate gains that tokenization promises are actually yours to keep.